If you've decided that a new home in on your radar, you may be hoping that waiting until next year will save you money. Everybody believes these crazy prices will come down, right?

I hate to burst your bubble, but prices are not coming down, and interest rates are going up. This is not a happy combination for buyers. This is your analysis:

Where will home prices be a year from now?

Where will mortgage rates be a year from now?

Where Will Home Prices Be a Year from Now?

Three major housing industry entities are projecting ongoing home price appreciation in 2022. Here are their forecasts:

Fannie Mae: 7.4%

Freddie Mac: 7%

Currently, the median home price in Silicon Beach sits at a hair over $1.5M (or more than 4x the median national price). Using an average of the three price projections above (6.5%), a home that sells for $1.5M today will be valued almost $100K higher at the end of next year. That's a significant chunk of change.

Where Will Mortgage Rates Be a Year from Now?

Today, Freddie Mac announced their 30-year fixed mortgage rate is at 3.1%. However, most experts believe mortgage rates will rise as the economy recovers, especially as a response to inflation. Here are the forecasts for the fourth quarter of 2022 by the same three major entities mentioned above:

Fannie Mae: 3.4%

Freddie Mac: 3.7%

That averages out to 3.7% if you include all three forecasts.

What It Means for You If Home Values and Mortgage Rates Increase

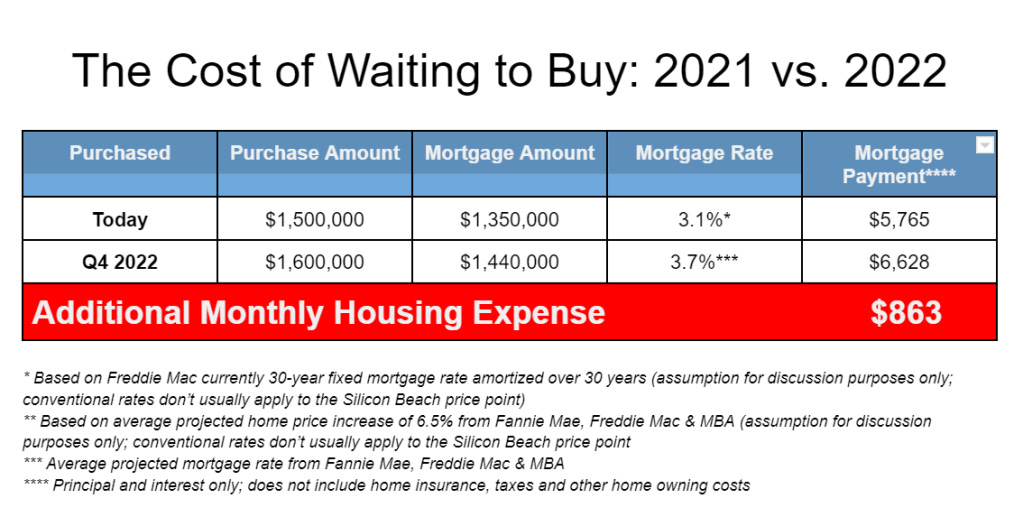

If both variables increase, you’ll pay a lot more in mortgage payments each month, but how much? Let’s assume you purchase a $1.5M home today with a 30-year fixed-rate loan at 3.1% (the current rate from Freddie Mac) after making a 10% down payment. According to mortgagecalculator.net, your monthly mortgage payment would be approximately $5,765 (this does not include insurance, taxes, and other home ownership costs).

That same home one year from now could cost $1,600,000 (in round numbers), and the mortgage rate could be 3.7% (based on the industry forecasts mentioned above). Your monthly mortgage payment after putting down 10%, would be approximately $6,628.

The difference in your monthly mortgage payment would be $863 every month. That’s $10,356 more per year and $310,680 over the life of the loan. You can take a really nice vacation every year on that $10,356.

Also consider that if you buy now rather than the end of next year, you will pick up an estimated $97,500 in forecasted equity next year, in addition to the $10,356 in mortgage savings for the year. Do you see why I keep banging the drum for buyers to act sooner rather than later. And this is just buying the median priced Silicon Beach home at $1,500,000. Many of my readers are shopping at higher price points.

Bottom Line

When asking if you should buy a home, the non-financial benefits of homeownership are what you want to think about. When asking when to buy, the financial benefits make it clear that doing so now is much more advantageous than waiting until next year. So who wants to see some houses? I'm working through the holidays.